Are IT Certification Fees Tax-Deductible in Australia? ATO Rules Explained

The ATO treats most certification costs as self-education expenses. Whether you can claim them depends on the connection between the study and how you earn your income right now.

IT certifications can be a solid way to stay employable in Australia's cloud and DevOps market, but the tax question comes up every year: can you claim the exam fee, training, and study materials as a deduction?

The short answer is "sometimes". The Australian Taxation Office (ATO) treats most certification costs as self-education expenses, and deductibility turns on whether there is a clear connection to how you earn your income right now.

Table of Contents

- 1. The ATO test: is there a clear connection to your current work?

- 2. Common IT certification scenarios, mapped to ATO outcomes

- 3. What expenses can fall under "self-education" for IT certs?

- 4. What the ATO usually will not allow

- 5. The 1 July 2022 change: the old $250 reduction is gone

- 6. Employer reimbursement, allowances, and "double dipping"

- 7. Mixed purpose study: apportionment matters

- 8. A practical checklist for deciding "claim or don't claim"

- 9. Record keeping the ATO expects

- 10. What to claim for IT cert prep (and what to leave out)

- 11. Where it goes in the tax return

- 12. If you are unsure, get a private view before you lodge

- 13. Frequently Asked Questions

The ATO test: is there a clear connection to your current work?

The ATO's starting point is practical: a self-education expense is generally deductible only when it directly maintains or improves the skills and knowledge you use in your current role, or is likely to increase your income in that same role. If the study is mainly to help you get a different job or enter a new field, it is usually not deductible.

That "work nexus" sounds simple, yet people get it wrong because they think "IT study is always relevant to IT work". The ATO looks for a tighter link than that.

A useful way to self-check is to write a one-paragraph explanation that connects your current duties to the certification's topics. If you cannot write that paragraph clearly, the claim is at risk.

Ask yourself:

- What tasks do I do now, week to week?

- Which parts of the certification map to those tasks?

- Is my goal a pay rise or progression inside the same occupation, rather than a career switch?

If you can answer those in plain language and back it with records, you are in a much stronger position.

Common IT certification scenarios, mapped to ATO outcomes

Even within IT, the purpose matters as much as the content. A Kubernetes exam might be strongly work-related for one person and non-deductible for another.

The table below gives a practical view of how the ATO rules often land in real life.

| Scenario (IT certification) | Likely deductible? | Why the ATO may accept or deny | Evidence that helps |

|---|---|---|---|

| You are a cloud engineer and sit AWS Solutions Architect to support designs you already deliver | Yes (often) | Maintains or improves skills used in current income-earning duties | Duty statement, project notes, exam invoice, course outline |

| You are a network admin and sit CCNA because your employer is moving to new routing gear | Yes (often) | Direct connection to current work tasks | Change plan, emails, job description |

| You are a junior sysadmin and complete Docker/Kubernetes certification to move into DevOps in the same employer | Maybe | Can be deductible if it increases income in the same employment stream and relates to current duties | Promotion pathway, performance plan, role expectations |

| You are in sales and study Azure certs to move into a technical pre-sales role next year | Risky | If it is really a new occupation, the nexus is weaker | Documented current technical duties help, not just future plans |

| You are changing careers (e.g. hospitality to IT) and pay for your first vendor cert | No (usually) | Study is to enable new employment, not to earn current income | Records will not fix the underlying issue |

| You pay a renewal fee required to keep working in a role that needs the credential | Yes (often) | Renewal maintains your ability to keep earning income in that job | Renewal notice, proof it is required |

The same certification can sit in different boxes depending on your current duties and why you incurred the cost.

What expenses can fall under "self-education" for IT certs?

Certification claims are not limited to the exam fee. The ATO's guidance on self-education expenses can include course fees and a range of related costs, as long as each item still meets the same work-related test.

People tend to claim the exam fee and forget the smaller items, or claim everything and hope for the best. A better approach is to treat each cost like a separate claim that needs its own work connection and records.

Typical claimable items (when the certification is work-related) include:

- Exam and assessment fees

- Paid training courses tied to the certification

- Textbooks and paid study guides

- Practice exam access fees

- Stationery and some printing costs

What you can claim also depends on whether the cost is private, capital, or has mixed use.

What the ATO usually will not allow (even if you work in IT)

The ATO's "no" decisions often come from one of three patterns: new job, too general, or not incurred while earning income in that role.

Here are frequent problem areas:

- New employment: Study that mainly helps you get a different job or enter a new field.

- Too general: Broad learning that is only loosely connected to your current tasks.

- Not the right timing: Costs incurred before you start earning income from the role the study relates to.

Common trap: There is also a frequent issue around initial licences or credentials. If the cost is an upfront requirement to start work (rather than to continue work), the ATO may treat it as not incurred in earning your income yet.

The 1 July 2022 change: the old $250 reduction is gone

If you remember older advice about "the first $250 is not deductible", that was linked to a provision that applied to self-education expenses in earlier years. That rule was repealed from 1 July 2022.

For recent tax years, that means you do not automatically lose the first $250 of eligible self-education costs. Your focus should be on the work connection and substantiation, not on trying to "get over the threshold".

Key change: From 1 July 2022, the $250 non-deductible threshold no longer applies. The full amount of eligible self-education expenses is deductible, subject to the usual work-related test.

Employer reimbursement, allowances, and "double dipping"

A clean rule: if your employer reimburses you, you generally cannot also claim the same amount as a deduction.

If you pay out of pocket and are not reimbursed, the claim is still only available if the certification relates to your current income-earning work. If you receive an allowance, the right treatment can depend on the facts and how it is reported on your income statement. Many people get this wrong, so it is worth checking how the payment is described and whether it was assessed as income.

Mixed purpose study: apportionment matters

IT study is often mixed. You might do a course that is half relevant to your current role and half aimed at a future move. Or you might buy a subscription that covers multiple certification tracks.

In those cases, you may need to apportion, claiming only the part that is sufficiently connected to your current duties. Apportionment is not about guesswork. It should be based on something you can explain and support, like course modules, hours spent on relevant units, or separate invoices.

Timing matters too. If you incur the expense while working in a role that needs the skills, the nexus is stronger. If you incur it before you start that role, the claim is more likely to be denied.

A practical checklist for deciding "claim or don't claim"

Before you lodge, treat the decision like an exam question: identify the rule, apply the facts, then gather evidence.

- Current duties: The certification maps to tasks you already perform (not just tasks you want to perform).

- Income link: You can show it helps you earn more in the same employment stream, or maintain required skills.

- Out-of-pocket cost: You paid and were not reimbursed.

- Records: You have invoices, course outline, and notes explaining the link to your role.

If one of those fails, the safest move is often to not claim, or to claim only a clearly work-related portion.

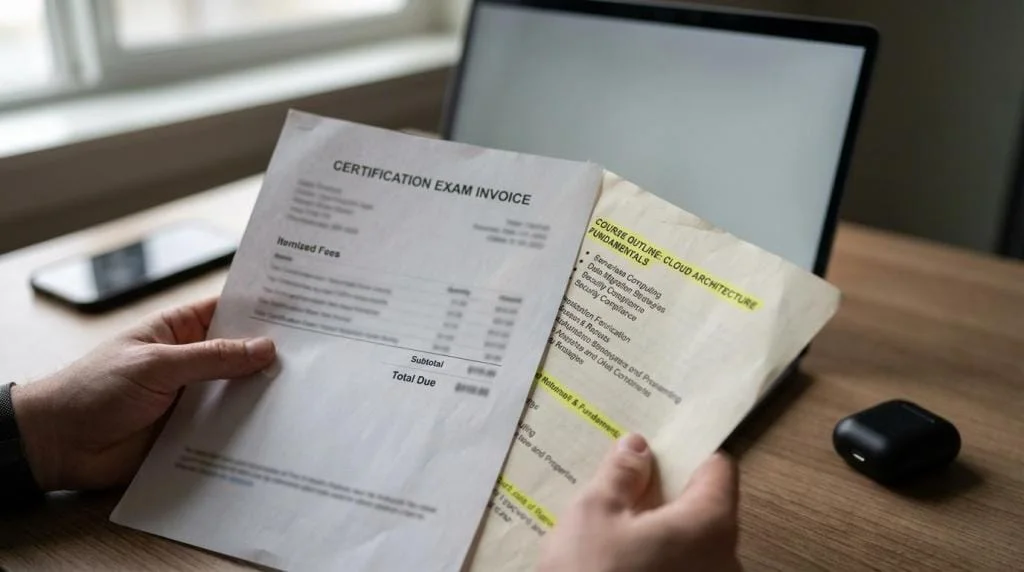

Record keeping the ATO expects (and what to save for cert exams)

The ATO is clear about substantiation: you should be able to show what you spent, when you spent it, what the course covered, and why it relates to your work.

That is straightforward if you treat your certification like a project and collect records as you go, rather than scrambling at tax time.

After paying for a certification, save:

- Receipts and invoices: Exam provider invoice, course provider receipt, card statement if needed.

- Course outline or syllabus: A PDF or screenshot that lists topics and learning outcomes.

- Work connection notes: A short document linking the topics to your role, plus a duty statement or job description.

Where claims fall over is rarely the lack of an invoice. It is the lack of a convincing story, supported by documents, that ties the expense to current income-earning activities.

What to claim for IT cert prep (and what to leave out)

IT candidates often buy a mix of learning resources: video courses, lab environments, practice exams, books, and sometimes new hardware. Some of those items can be deductible, some cannot, and some require apportionment.

Quick wins (usually straightforward to claim)

- Exam fees

- Practice question access

- Certification renewal fees

Grey areas (may need apportionment)

- Subscriptions, bundles, and platforms that cover multiple tracks where only part relates to current duties

Usually not claimable

- Private expenses, entertainment, or general-purpose items with no clear work link

If you use a mobile-first prep platform (including practice exam apps and study guides from providers like ExamCert), the tax question is not about the brand. It is about whether the content supports skills you use in your current role, and whether you can substantiate the purchase and purpose.

Where it goes in the tax return (and how to describe it)

For employees, self-education expenses are typically claimed in the work-related self-education section of the return (often labelled at D4 in ATO instructions). Tax agents may label it slightly differently in software, but the category logic is the same.

How you describe the claim matters. "IT course" is vague. A clearer description ties it to your role, like "AWS certification exam fee and course, cloud engineer role".

Consistency matters: Keep your wording factual and consistent with your documentation. If your records say you are a service desk analyst and your description says you claimed it as a cloud architect, expect questions.

If you are unsure, get a private view before you lodge

Some situations are genuinely borderline: moving from IT support into cybersecurity within the same employer, doing a cloud certification while transitioning roles, or studying a broad program with only partial relevance.

If your facts are complex, it can be worth speaking with a registered tax agent, or checking the ATO's self-education guidance directly and saving a copy of the relevant page for your records. A cautious approach is often cheaper than fixing a claim after an ATO review.

Disclaimer: This article is general information only and does not constitute tax, financial, or legal advice. For guidance on your specific circumstances, consult a registered tax agent or the ATO directly.

Frequently Asked Questions

Can I claim IT certification exam fees on my Australian tax return?

Yes, if the certification directly relates to your current employment. The ATO treats exam fees as self-education expenses, which are deductible when they maintain or improve the skills you use in your current role. You must have a clear connection between the certification content and your current duties.

Is the $250 self-education expense reduction still in effect?

No. The $250 non-deductible threshold for self-education expenses was repealed from 1 July 2022. For recent tax years, the full amount of eligible self-education costs can be claimed, provided they meet the ATO's work-related test.

Can I claim a certification if I'm changing careers into IT?

Generally no. The ATO requires self-education expenses to relate to your current income-earning activities. If you are studying to enter a new field (e.g. from hospitality to IT), the expense is usually not deductible because the study is to enable new employment, not to earn your current income.

What records do I need to keep for IT certification tax claims?

Keep receipts and invoices for all expenses, a course outline or syllabus showing what the certification covers, and a short document linking the certification topics to your current role. A duty statement or job description strengthens your claim. Save these records as you go rather than at tax time.

Can I claim both the exam fee and study materials?

Yes. If the certification is work-related, you can claim exam fees, paid training courses, textbooks, practice exam access fees, and relevant stationery. Each item must independently meet the work-related test and be substantiated with records.

What if my employer pays for the certification?

If your employer reimburses you for the cost, you generally cannot also claim the same amount as a deduction. If you receive a study allowance, check whether it was included as assessable income on your payment summary. The treatment depends on how the allowance is reported and structured.

Preparing for an IT Certification Exam?

ExamCert offers free practice questions for AWS, Azure, GCP, and security certifications

Start Free PracticePlan Your Study Journey

Use our free tools to optimize your preparation